Taking risk can be rewarding, even for a bank

"How much risk are you prepared to accept?"

I picked up a line from now-retired Vice-Admiral’s Mark Norman and Ron Lloyd that you’ll find is applicable in most facets of your professional and personal life: "How much risk are you prepared to accept?"

According to my morning New York Times, one of the top stories of 2023 was the series of Regional bank failures that began with the collapse of Silicon Valley Bank (SVB) back on March 10th, which it described as the “biggest bank failure since the 2008 financial crisis”:

A recap: The bank’s clients — spooked by news that the bank was working to shore up its finances and that Moody’s had downgraded its bond rating — had pulled out more than $40 billion of their deposits. On March 12, regulators shut down Signature Bank, a New York-based lender.

The banks’ failures led to fears about the stability of other midsized lenders. Wall Street’s biggest banks agreed to give $30 billion to First Republic and Swiss authorities brokered a deal for UBS’s to take over of its domestic rival, Credit Suisse. But even a multibillion-dollar intervention wasn’t enough to save First Republic: Federal regulators seized the lender in May sold it to JPMorgan Chase.

As someone who had competed against the team at SVB for more than two decades, and admired what they’d built at each step along the way, the timing was fascinating. It had only been a month since I’d announced my decision to leave CIBC following the 5th anniversary of Wellington Financial’s acquisition (see prior post “Time to chart my next Adventure” Feb 2-23), and the most unexpected situation had come to pass. Twelve months ago, I’d have told you that it would be more likely that my Dad and I would win the LottoMax than it would have been for SVB to go under in the course of a few days.

A reminder as to why I’m not qualified to provide stock picks, even if I was 25 times better at it than Kevin O’Leary over a six-plus year period (see prior post “Decade of Daddy Mirror Fund goes to cash” Oct 14-14).

Although it had nothing to do with the credit quality of the innovation economy, SVB’s very sudden demise — after 30 years of hockey-stick-type results — has undoubtedly negatively impacted the external view of the Tech, Life Science and Clean Tech ecosystem as an attractive place to lend money: Regulators will believe they now have to pay much more attention to commercial banks with an exposure to the space, and the Doubting Thomas’s at various bank Risk Departments will claim that SVB’s collapse proves that they were prescient to have steered clear previously.

When CIBC created it’s own organic Tech lending offering in 2016, the sector was a beacon of opportunity. Awash in sticky deposits and generating outsized loan growth, you’d think that a multitude of North American commercial banks would be all over the sector.

Not so, in fact.

While the Canadian banking fraternity had long-since figured out how to lend against the value of a lobster fishery licence held by a Fisher from Cheticamp, N.S., it was either unable or unwilling to ascribe a value to a fast-growing, VC-backed, cashflow negative software company based in Etobicoke, Ontario. Despite the fact that RBC’s Knowledge-Based Industries group had a national brand and deposit base of 1,000+ clients, it was U.S.-based tech and life science lenders Comerica and SVB that had been dominating the bank Tech / Life Sci lending market on this side of the 49th parallel for the entire 21st century.

In the months that followed taking the reins as CIBC CEO in September 2014, Victor Dodig heard a similar refrain from Tech entrepreneurs in Waterloo, Vancouver, Montreal and elsewhere: “Why can’t I borrow money from my local bank?”

With his keen eye and client-focussed mindset, Mr. Dodig saw the broad success that SVB was enjoying as a true lender, supporter of the innovation ecosystem and highly-sought public company: Fast growth, very low average loan losses, self-funding, and a premium trading multiple. It is to his great credit that he turned to his Commerical banking leader Jon Hountalas, SVP Blair Cowan and the Corp Dev. team and encouraged them to try to rise to the challenge of all of the Tech entrepreneurs who’d been imploring him (and the rest of the Big 5 banks) to meet their multiple needs.

I won’t bore you with the zigs and zags of the acquisition process as they’re not relevant to my larger point, beyond the success that our group achieved over the five years that followed CIBC’s acquisition of Wellington Financial on Jan. 8/18. That we successfully managed to build a fast-growing regulated business in 14 different markets during Covid, and committed more than $10 billion dollars to the ecosystem before I’d left, was a collective success. Hundreds upon hundreds of people in a variety of roles (AML, Brian McDonough {Risk}, HR, IT, Investment Banking, Portolio Mgmt., Wealth Mgmt., etc.) all played a constructive role in the build-out, and we overcame the very hurdles (cross-border jealousy, Comms) and nay-sayers you’d expect along the way.

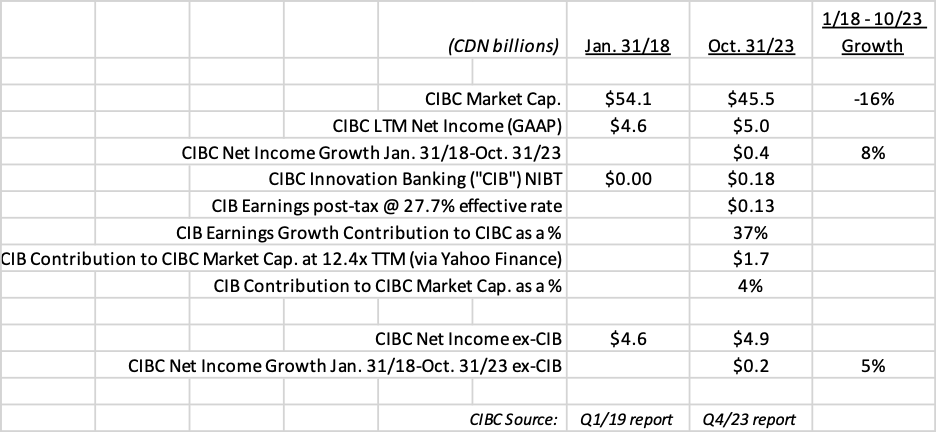

As you can see below, CIBC’s shareholders benefitted meaningfully from this collective effort. According to CIBC’s disclosure, CIBC’s Innovation Banking group generated ~37% of the overall bank’s GAAP net earnings growth between Jan. 31/18 and Oct. 31/23 (the end of the 2023 fiscal year). Note that reported GAAP earnings are lower than “adjusted earnings” by ~$1.5B for fiscal 2023 ($844M of that adjustment relates to a legal settlement in 2023, for example) but they’re apples-apples for this purpose:

On an adjusted earnings basis, the group’s contribution to after-tax earnings between the periods in question comes in at a much more modest ~11%, which is still a reason for shareholders to get up in the morning. As a creator of CIBC shareholder value, to contribute 3-4% of the market cap. of a 150 year-old bank’s total value after five short years speaks to the materiality of the opportunity.

If the deal had never closed, there’s at least one senior banker who’d want me to remind you that the bank capital we used to advance those Tech and Life Science loans would have been put to work by another line of business instead, so it’s not as though no additional earnings would have been generated by other CIBCers. That’s true, but our group raised more in deposits than we distributed in loans, unlike most (Ed note: All, surely!) other commercial banking niches. You can’t lend dollars that you’ve not raised in the form of deposits from somewhere, no matter how much regulatory capital you have available to leverage.

The point of this is not to brag, but to encourage the Regulatory World to take notice of the tangible opportunity; to “accept the risk” associated with the space. And to act — the Innovation Economy needs you to encourage your Charges to grow their loan exposure to the space, and there’s plenty of business to go around. Whenever we lost a deal to a new entrant, even if they were a Pretender, my response was always the same: “this is good for the sector!”

As we approach the sixth anniversary of CIBC’s big splash, the only question is: why haven’t other large banks tried harder to replicate this financial success? Plenty have a dedicated team, but the number of actual company loans advanced in any given quarter is often pitiful. Some bank groups seem prepared to spend more time and money each year on marketing their offering than they actually commit to true venture debt deals. That might be good for GR purposes and DEI buzz, but it doesn’t pay shareholder dividends.

The next few years are unlikely to generate meaningful volumes in the real estate sector, for example, and Scotiabank’s foreign market experiences have been hit-and-miss over the past 25 years. BMO went all-in on Mexico in the 1990’s, and it’s now clear that CEO Darryl White recognizes the Gold Mine represented by places that are a bit closer to home: California and the U.S. Southwest — in keeping with a component of former Chairman Matt Barrett and Vice-Chairman Jeff Chisholm’s earlier expansion strategy: “following the Snowbirds.”

I’d have some questions if I was a Board member of a large commercial bank that actively tracks our institution’s quarterly efforts to be “Net Zero” by 2030 or 2050, but we’re not doing much — if any — lending to the Clean Tech sector. How do we expect entrepreneurs to solve these difficult global carbon challenges without access to a key traditional form of capital? As for Tech and Life Science, I can’t think of a single traditional midsize or large bank that has a drawn loan exposure that reflects either vertical’s contribution to GDP in Canada, the USA, UK or Germany.

All of which leads to less innovation, lower job creation and diminished economic growth. Someone needs to lead the way, whether it be Politicians, Regulators, Insitutional Shareholders or Bank Boards / Executives. Bloggers can only “shout at the sky.”

The status quo isn’t working for anyone, unless you’re prepared to accept mediocrity. If our small team could pull it off, anyone can!

MRM

Note: this post, like all blogs, is an Opinion Piece

Photo: Seamstress Fitter, London, 1950, by Irving Penn