Private Credit gets sideswiped by the "SaaS-Pocalypse"

"It’s the End of the World as We Know It (and I Feel Fine)"

The run to $2 Trillion under management has been absolutely incredible, but if “Private credit’s ‘golden era’ started to show signs of tarnish” in 2024, the mood is now as dark as it’s ever been. For reasons that aren’t entirely coherent, market commentators seem to fear that advances in artificial intelligence are going to gut the tech component of loan books of various private credit fund managers.

This unsubstantiated groupthink reminds me of the early days of 2000, just as the NASDAQ crashed: “It’s the End of the World as We Know It.” Valuations had good reason to come-off back then, predicated solely on “eyeballs” in some cases, but the notion that the sector was toast for all-time was laughable. Today’s Equity Analysts are welcome to moderate their outlook for tech earnings, for that’s their call — but I’d like to meet the person who’s done the work that demonstrates that these profitable (or fast-growing and currently unprofitable) businesses are all going bankrupt over the next decade.

As someone who is currently speaking to institutional investors about what I believe are very appealing opportunities in the innovation private credit space (via my newly-formed Wellington Growth Partners, Inc.), any negative sentiment in the public markets is bound to stimulate questions about what AI means for your garden variety software company. Concerns abound, and for good reason. Some publicly-traded SaaS names, such as Workday (WDAY:Q), are down ~40% so far this year, as slower growth, tighter margins and chatter that AI is going to somehow make the company obsolete have led to contracting valuations.

Putative advances in AI are giving CFOs the upper hand when the time comes to negotiate renewals on their payroll, HR, CRM and other backbone software platforms; just as the GFC turmoil temporarily shifted power from seller to buyer in 2009-10.

Private credit CEOs, such as Orchard Global’s (US$8.6B AUM) Paul Horvath, are taking to CNBC to assure investors that his firm likes to play in the “asset heavy” sectors, while staying “away from those asset-light industries.” When asked if his firm is still lending to tech firms, Blue Owl’s Craig Packer recently told CNBC that his firm is “being super selective.”

As Wellington Financial’s LPs would attest, if you want to be successful as a tech lender over the long haul, being “super selective” is a key success factor (see representative prior post “Preqin names Wellington Financial to list of “Most Consistent Top Performing” funds” Oct. 24-16). That’s not been the case of late. With ever-expanding multiples and consistent equity flows into the sector (VCs and Growth Equity investors have invested US$1.97T into U.S. Start-ups and growth stories over the past decade), lending to software firms has been a lay-up over the past five years. When something looks easy in the credit space, and incremental management fees are there for the taking, you’re going to draw plenty of tourists.

“There are going to be winners and losers in private credit,” says Mr. Horvath, which might call for new “guard rails” to protect retail investors. Market Technicians, such as Piper Sandler’s Chief Craig Johnson, seem to be staying clear of publicly-listed private credit managers.

The perceived looming crisis is such that Op-eds are now warning investors to “Beware the private-credit dark money infecting Wall Street.”

The private-credit sector has been described as a private junk-bond market, providing high-interest loans to steeply leveraged, unlisted companies, often unprofitable software startups.

___

The biggest problem with private-credit funds is that they operate largely in the dark, providing investors limited disclosure and no real-time public pricing (regulated BDCs are more transparent). The value of their assets at any moment is whatever the manager says it is, based on internal analysis and outside consultants. That, says Moody’s, makes “it difficult to assess the underlying risks.”

That should be enough to make you hit the sell button, for fear that the Global Financial calendar has been turned back to February 2008.

Team by team reporters, baffled, trumped, tethered, cropped, look at that low playing, fine, then. (Lyrics: Michael Stipe, REM)

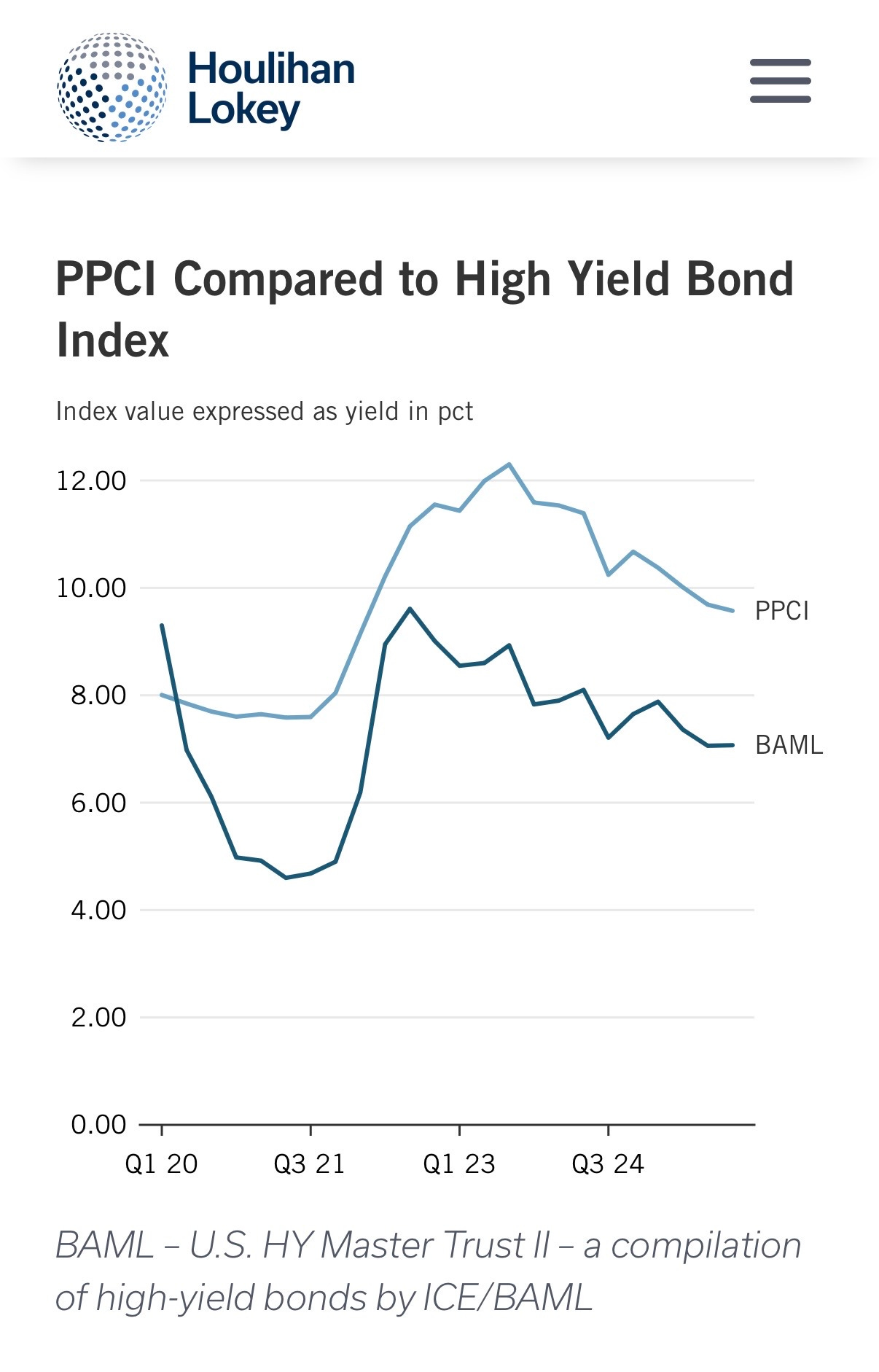

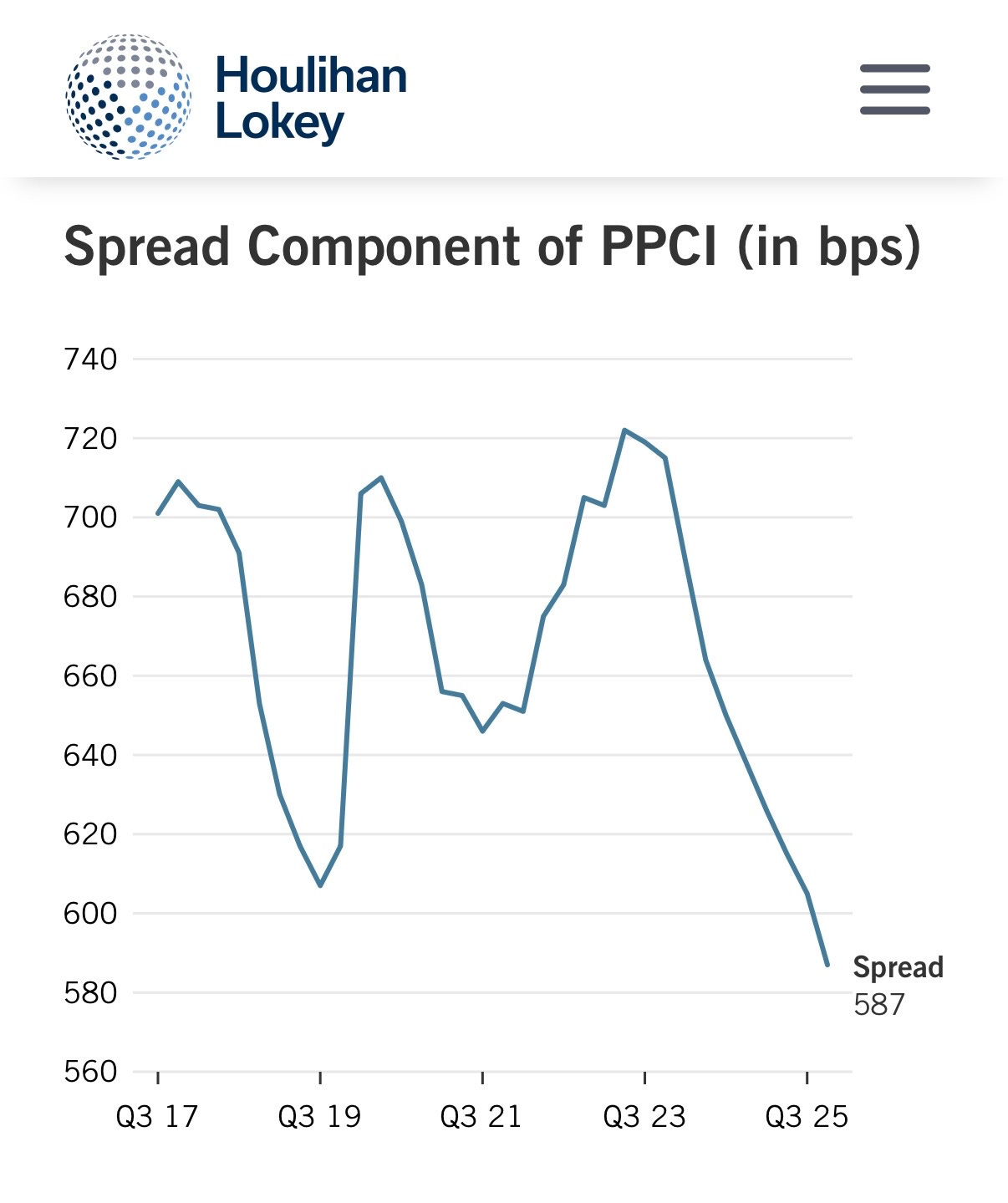

My PA continues to be long banks and tech, so I’d hope that I’m not looking at this with rose-coloured glasses. That rating agencies aren’t yet screaming isn’t determinative, given their pre-GFC track record, but there’s nothing in the Houlihan Lokey private credit index, nor the more traditional high yield bonds, telegraphing that a major credit crisis is in the offing:

What gives, you ask?

The combination of both the heft and genius of JP Morgan’s Jamie Dimon was on full display last October when, in the wake of two high profile U.S. bankruptcies, he warned shareholders that there were more blow-ups to come. Investors, Analysts and business media heard him loud and clear. En masse, they seemed to conclude that the risk wasn’t in the banking sector, but in the “opaque” private credit market.

Despite the fact that private credit funds held only small slivers of TriColor ($900M) and First Brands ($10-11B) secured / off-balance sheet debt. An S&P Global Ratings Analyst told CNBC’s Squawk Box Europe the other morning that “so far, credit fundamentals are good at the BDCs. We’ve run some stresses on them and they are solid.” And yet, shares in private credit firm Blue Owl (OBDC:NYSE) are off 22% over the past twelve months.

Blue Owl did sell US$1.7B of their loan portfolio at 99.7 to four other lenders a few days ago, which served to demonstrate the quality of that particular list of individual credit exposures. And it also provided enough cash to satisfy the demands of various investors who were asking for some/all of their capital back. There’s an obvious mismatch when investors put money into a credit fund — which in turn deploys that capital via a 5-year loan to a company — only to change their minds a year later and wonder why they can’t just get their capital back when they want it. Because we put it into a company at 10%, like you asked, is why.

When you look at the next chart, you get some insight into what might be pissing off senior bank executives. The “huge” growth in the private credit market over the last two years is being blamed by some for weaker structures and lower spreads:

It’s a volatile market, as you can see above. Spreads might be down because private credit managers are mis-pricing risk, or they’ve simply moved so far up-market that it’s only natural that spreads would get tighter as the credit quality of the borrowers improved. Or a bit of both, which is why banks like BoA, JPM and Wells Fargo have wisely made their own inroads in the asset class.

The doubters point out that “Moody’s worries that competition in the sector will encourage looser lending standards, and expects that private-credit funds ‘will likely be more central in the financial system in future stress periods’ and large banks less so. ‘In other words, the locus of contagion has shifted toward nonbank lenders, including private credit.’” Ashok Bhatia, Chief Investment Officer at Neuberger Berman, indirectly refutes the point, at least as far as the First Brands and Tricolor deals are concerned: “that the drivers of the issues at these two companies were idiosyncratic in nature.”

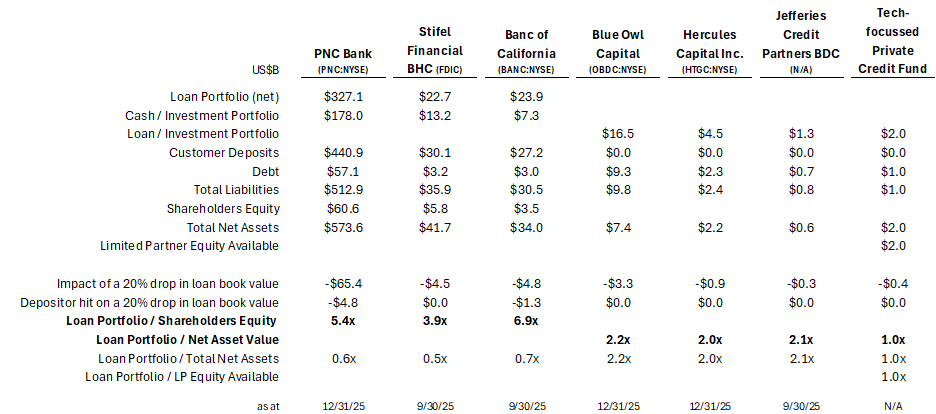

As large as the private credit market has become, I just don’t see the systemic risk it represents. An aggregate global capital pool of US$2 trillion sounds like a lot, but that merely represents the loan book of a single large bank, such as Citi (C:NYSE). And those Citi loans are largely funded by customer deposits, unlike private credit facilities, which are funded by limited partnership commitments from institutional investors, such as pension plans, Sovereign Wealth Funds and life insurance companies.

In the table below, you’ll see why that’s important.

PNC Bank, a very credible lender to growth companies in the tech sector, has a US$327B loan book across a countless individual and commercial entities, but “only” US$60.6B of equity capital. If anyone is worried about “leverage,” PNC’s ratio is 5.4x. Over at Blue Owl’s BDC, the loan book was just 2.2x the firm’s “net asset value.” And, importantly, no customer deposits are involved, unlike PNC, BANC or Stifel’s FDIC-insured venture banking arm, for example.

If Mr. Market was truly worried about Late-stage software loans going sour, I can’t believe PNC shares would have been up 19% over the past twelve months.

I don’t want to leave you with the impression that every VC-backed Innovation story is going to work out. Take Montreal-based Sheertex, which is in the process of completing an insolvency sale:

In a filing with Quebec Superior Court, the company said that despite raising more than US$200-million since its founding in 2017, by last fall SRTX was struggling with limited financial resources after encountering multiple challenges, including high production costs, delays in scaling the company, the cyclical nature of the hosiery sector, exchange rate fluctuations “and shifting trade policies” that “collectively contributed to the applicants’ cash flow challenges.”

Montreal-based SRTX raised US$37.5-million last year from existing investors including H&M Group, BDC Capital, Export Development Canada and Investissement Québec and hired a new chief executive officer in September to replace founder Katherine Homuth. The new funding was supposed to give SRTX enough cash to fund a planned production expansion.

But liquidity issues continued, and the replacement CEO, retail and fashion veteran Sophie Boulanger, departed after less than two months as the board put SRTX up for sale in October. (via G&M)

Talented management, a market vision, customer take-up and hundreds of millions of dollars of equity investment are no guarantee of success. That’s how it’s always been in the innovation economy, dating back at least to Wellington’s first loan transaction in August 2000. I don’t wish ill on the beneficiaries (via the LPs) of any particular private credit firm, but, if there’s pain to be felt within the tech lending world, bring it on.

When times get tougher, entrepreneurs, VCs and LPs alike both need and deserve experienced lenders. We saw that circa 2000-2004, 2008-09, 2016, March-August 2020, and most certainly in the months and years to come.

As Warren Buffet famously reminds: “Only when the tide goes out do you discover who's been swimming naked.” The ocean isn’t the issue, in his metaphor, it’s the absence of protective bathing suits.

MRM

(notes: this post, like all blogs, is an Opinion Piece; for the new readers, CIBC acquired my former firm Wellington Financial LP in 2018)

(disclosure: I’m not licenced to give financial advice, and this post is not an offering to sell securities)